The number: $1,765 per week

If you file a PFL claim in 2026, the most California will pay you is $1,765 per week. That's gross, before taxes. Over the full 8 weeks of PFL, that works out to $14,120 total.

This number comes from EDD and it changes every January. In 2025 it was $1,620, so the 2026 cap went up by $61. EDD ties the increase to statewide average wages, though they don't publish the exact formula for the cap adjustment itself (the benefit calculation formula is public, the cap-setting math is not).

The same $1,765 cap applies to State Disability Insurance (SDI) too, since PFL and SDI run on the same formula.

How the cap actually works

The cap kicks in at ~$124,800/yr. Max 8-week total payout: $14,120

The cap isn't a separate rule on top of the formula. It's built into the math. Here's what happens when EDD calculates your benefit:

They find your highest-paid quarter in the base period (the 12 months ending 5 to 18 months before your claim). They divide that quarter's wages by 13 to get your average weekly wage (AWW). Then they multiply by 70% if your AWW is above $1,252, or 90% if below.

The result of that calculation simply can't exceed $1,765 because the wage base has a ceiling. Once your highest quarter earnings hit roughly $31,200, the math plateaus.

What salary hits the cap?

If your pay is spread evenly across the year, you need to earn about $124,800 annually to max out PFL.

$124,800 / 4 quarters = $31,200 per quarter. $31,200 / 13 weeks = $2,400 AWW. $2,400 x 70% = $1,680. That's basically the cap (the $1 difference is rounding).

Earn $130,000? You still get $1,765. Earn $200,000? Same $1,765. Earn $500,000? Still $1,765. The cap doesn't care.

One exception: if your income is uneven across quarters (big commission in Q2, slow Q4), you might hit the cap at a lower annual salary because one quarter was unusually high. Or you might miss it at a higher salary because your best quarter wasn't good enough.

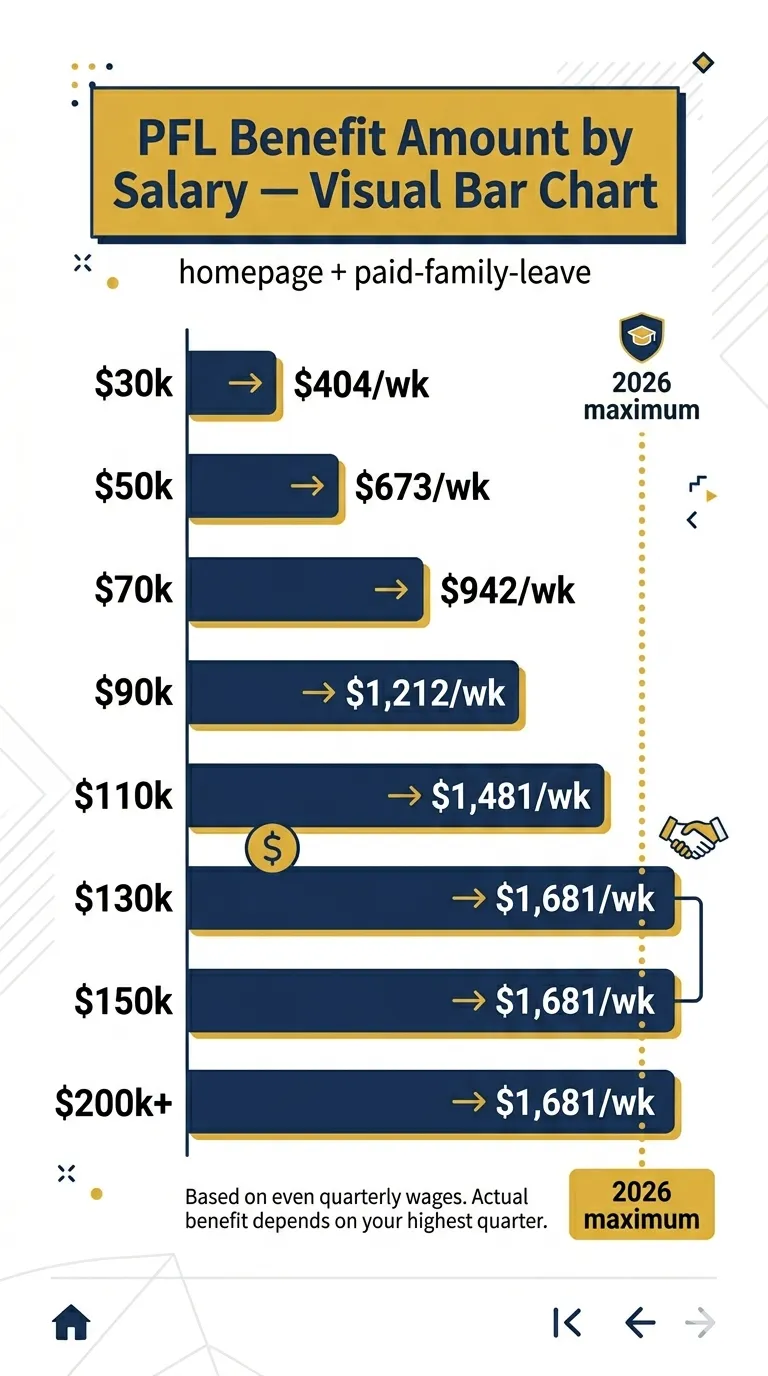

PFL benefits at every salary level

Weekly benefit at each salary level (2026)

Here's what the weekly benefit looks like at different annual salaries, assuming even pay throughout the year:

| Annual salary | Highest quarter | AWW | Rate | Weekly benefit | 8-week total |

|---|---|---|---|---|---|

| $30,000 | $7,500 | $577 | 70% | $404 | $3,231 |

| $40,000 | $10,000 | $769 | 70% | $538 | $4,308 |

| $50,000 | $12,500 | $962 | 70% | $673 | $5,385 |

| $60,000 | $15,000 | $1,154 | 70% | $808 | $6,462 |

| $70,000 | $17,500 | $1,346 | 70% | $942 | $7,538 |

| $80,000 | $20,000 | $1,538 | 70% | $1,077 | $8,615 |

| $90,000 | $22,500 | $1,731 | 70% | $1,212 | $9,692 |

| $100,000 | $25,000 | $1,923 | 70% | $1,346 | $10,769 |

| $110,000 | $27,500 | $2,115 | 70% | $1,481 | $11,846 |

| $120,000 | $30,000 | $2,308 | 70% | $1,615 | $12,923 |

| $124,800+ | $31,200+ | $2,400+ | 70% | $1,765 | $14,120 |

The table makes one thing obvious: the gap between $120k and the cap is only $66 per week. If you earn $120,000, you're already getting 96% of the maximum.

What changed from 2025

Not much, honestly. Two things changed on January 1, 2026:

The weekly cap went from $1,620 to $1,765. And the SDI withholding rate changed. In 2025 California removed the taxable wage ceiling for SDI, which means there's no income limit on what you pay in. You pay SDI tax on every dollar you earn. But the benefit cap remains, so higher earners pay more into the system without receiving higher benefits.

The 70%/90% wage replacement rates themselves did not change. What did change is the AWW threshold separating the two tiers: it rose from $517.69 in 2025 to $1,252 in 2026 (the threshold is recalculated annually based on the State Average Weekly Wage). If your AWW is at or below $1,252 (roughly $65,000 annual salary), you get 90% instead of 70%.

| Detail | 2025 | 2026 |

|---|---|---|

| Maximum weekly benefit | $1,620 | $1,765 |

| Maximum 8-week total | $12,960 | $14,120 |

| Salary to hit cap | ~$120,120 | ~$124,800 |

| 70%/90% AWW threshold | $517.69 | $1,252 |

| SDI wage ceiling | None | None |

Three things people get wrong about the cap

"My salary is $130k so my benefit is 70% of $130k"

No. PFL doesn't take 70% of your salary. It takes 70% of your average weekly wage, which is calculated from your single highest-paid quarter. These are different numbers, and the result is capped at $1,765 regardless.

"I got a raise last month, so my PFL will be higher"

Probably not. The base period ends 5 to 18 months before your claim start date. If you got a raise 2 months ago, those higher wages likely fall outside your base period. EDD doesn't use your current salary. They use historical wage records from a specific 12-month window.

This catches a lot of people off guard. You can check your actual base period wages by logging into myEDD before you file.

"The cap means I lose money"

Sort of, but it's how insurance programs work. If you earn $200,000, PFL replaces about 44% of your income ($1,765 / $3,846 weekly). If you earn $60,000, PFL replaces 70% ($808 / $1,154 weekly). The legislature built PFL to replace a bigger share of income for lower-wage workers.

Some employers top up PFL with supplemental pay. San Francisco actually requires it for new-parent bonding leave at companies with 20+ employees through the Paid Parental Leave Ordinance. If your employer has a similar policy, the cap matters less.

"PFL is 8 weeks for everyone"

8 weeks is the maximum, not a guarantee. You can take fewer weeks. You can also take PFL intermittently, a few days at a time, though EDD's intermittent claim process is clunky and your employer may push back. The 8-week clock resets every 12 months.

If you earn less than $124,800

Most California workers do. The median household income in California was around $91,000 in 2024 (Census Bureau). At $91,000, the weekly PFL benefit is approximately $1,231, which is $450 less than the cap.

If your income is below $27,000 annually, you fall into the 90% tier instead of 70%. That means a worker earning $25,000 gets about $433 per week (90% of their $481 AWW), compared to $337 at 70%. The 90% rate exists specifically so lower-wage workers can afford to actually take leave.

The 41-day filing deadline is hard. You must file your PFL claim at edd.ca.gov within 41 days of your first day of leave. Miss it and you forfeit benefits permanently. There is no extension.

This article is for informational purposes only and is not legal advice. Benefit amounts are estimates based on the EDD formula. Your actual PFL benefit is determined by EDD from your official wage records. Sources: EDD PFL benefit amounts, EDD 2026 rates.